Financial planners have used this 4 rule for decades to estimate safe retirement spending amounts. However, its inventor claims that current market conditions make forecasts difficult. The inflation rate currently hovers at 8.5%, and the stock and bond market are highly valued making it harder to make accurate predictions about future returns.

4% rule

The 4% rule is a good starting point when it comes to retirement planning. Although the formula doesn't require you to invest all your money in stocks it can help you calculate your retirement income. Remember that the 4 percent rule assumes you have a 50/50 mixture of bonds and stocks. This may not always be true, as risk tolerance is different for each individual.

Another problem with the 4% Rule is that it assumes an annual constant rate of return. This assumption is absurd as the stock market doesn't always rise. This could mean that your retirement funds won't grow as much as they would like. Morningstar researchers claim that the current 4% rule should be changed to 3.3%. This is a more realistic number for most retirees.

The disadvantages associated with the 4% rule

The 4% Rule may not be the best method for retirement savings as it doesn't account for changes to spending patterns. Retirement savers tend to spend more on travel and hobbies in their early years. Their spending drops in the middle of their lives and then increases as they get older due to expensive healthcare expenses. These changes in lifestyle are not considered by the four rule. It also limits the amount of money a taxpayer can withdraw to retirement accounts.

This rule is outdated and does not take into account market conditions. For example, if a recession is underway, you might need to reduce your withdrawals, while in a good market, you may be able to comfortably withdraw more money.

Alternatives to the 4 percent rule

If you are looking for a conservative way to invest in retirement, you might want to look into alternatives to the standard 4% rule. The 4% rule was originally designed to incorporate market volatility, but it's a flawed strategy today. Instead of a conservative strategy, it recommends an aggressive asset allocation, which is typically 50-75% stocks.

In other words, you might choose to withdraw 7% rather than 4% the first year of retirement. This strategy doesn't account for the changing market. That means that your withdrawals during a downturn will be lower than your withdrawals during a good market. Even though the 4% rule assumes a 30-year period, your portfolio might not last that long. The 4% rule does not take into consideration the performance of your portfolio on the market.

FAQ

How old should I start wealth management?

Wealth Management should be started when you are young enough that you can enjoy the fruits of it, but not too young that reality is lost.

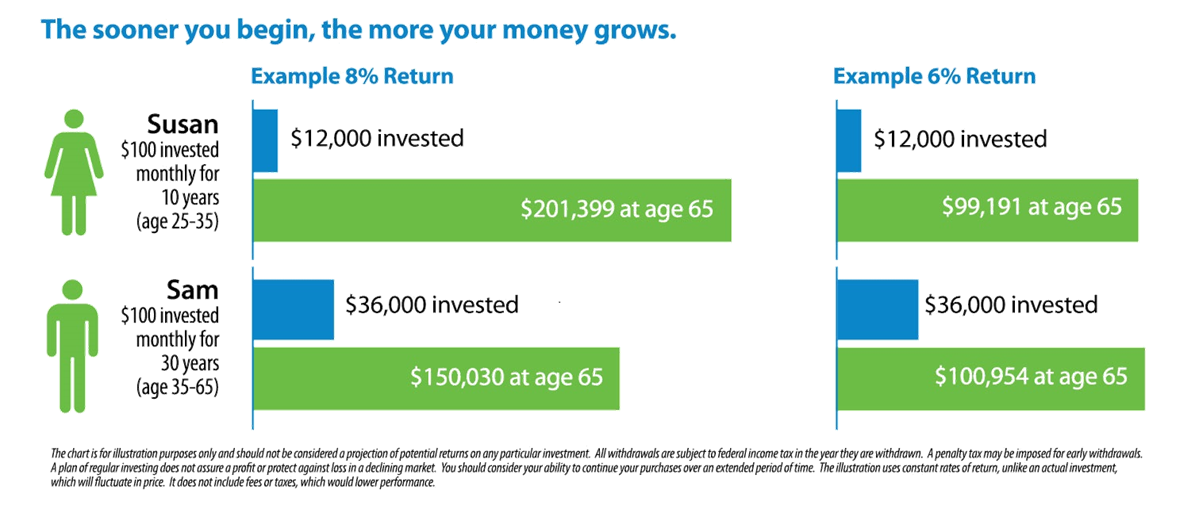

The sooner you invest, the more money that you will make throughout your life.

If you are thinking of having children, it may be a good idea to start early.

Savings can be a burden if you wait until later in your life.

What are some of the benefits of having a financial planner?

Having a financial plan means you have a road map to follow. It will be clear and easy to see where you are going.

It will give you peace of heart knowing you have a plan that can be used in the event of an unexpected circumstance.

A financial plan can help you better manage your debt. Knowing your debts is key to understanding how much you owe. Also, knowing what you can pay back will make it easier for you to manage your finances.

Protecting your assets will be a key part of your financial plan.

What is retirement planning?

Retirement planning is an essential part of financial planning. It helps you plan for the future, and allows you to enjoy retirement comfortably.

Retirement planning includes looking at various options such as saving money for retirement and investing in stocks or bonds. You can also use life insurance to help you plan and take advantage of tax-advantaged account.

What are the best ways to build wealth?

Your most important task is to create an environment in which you can succeed. You don’t want to have the responsibility of going out and finding the money. You'll be spending your time looking for ways of making money and not creating wealth if you're not careful.

Avoiding debt is another important goal. It is tempting to borrow, but you must repay your debts as soon as possible.

You can't afford to live on less than you earn, so you are heading for failure. If you fail, there will be nothing left to save for retirement.

Before you begin saving money, ensure that you have enough money to support your family.

What Are Some Examples of Different Investment Types That Can be Used To Build Wealth

There are many types of investments that can be used to build wealth. These are just a few examples.

-

Stocks & Bonds

-

Mutual Funds

-

Real Estate

-

Gold

-

Other Assets

Each of these options has its strengths and weaknesses. For example, stocks and bonds are easy to understand and manage. However, they can fluctuate in their value over time and require active administration. However, real estate tends be more stable than mutual funds and gold.

Finding the right investment for you is key. Before you can choose the right type of investment, it is essential to assess your risk tolerance and income needs.

Once you've decided on what type of asset you would like to invest in, you can move forward and talk to a financial planner or wealth manager about choosing the right one for you.

Statistics

- US resident who opens a new IBKR Pro individual or joint account receives a 0.25% rate reduction on margin loans. (nerdwallet.com)

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

- A recent survey of financial advisors finds the median advisory fee (up to $1 million AUM) is just around 1%.1 (investopedia.com)

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

External Links

How To

How do I become a Wealth advisor?

A wealth advisor can help you build your own career within the financial services industry. This profession has many opportunities today and requires many skills and knowledge. If you possess these qualities, you will be able to find a job quickly. The main task of a wealth adviser is to provide advice to people who invest money and make decisions based on this advice.

The right training course is essential to become a wealth advisor. It should include courses on personal finance, tax laws, investments, legal aspects and investment management. After you complete the course successfully you can apply to be a wealth consultant.

These are some helpful tips for becoming a wealth planner:

-

First of all, you need to know what exactly a wealth advisor does.

-

Learn all about the securities market laws.

-

You should study the basics of accounting and taxes.

-

After completing your education, you will need to pass exams and take practice test.

-

Finally, you need to register at the official website of the state where you live.

-

Apply for a work permit

-

Give clients a business card.

-

Start working!

Wealth advisors usually earn between $40k-$60k per year.

The location and size of the firm will impact the salary. If you want to increase income, it is important to find the best company based on your skills and experience.

We can conclude that wealth advisors play a significant role in the economy. Everybody should know their rights and responsibilities. Additionally, everyone should be aware of how to protect yourself from fraud and other illegal activities.